Construction Mortgages & Construction Loans: From Empty Lot to Move-In

If you can’t find the house you want, you either renovate or you build. Renovations have surprises. New construction has banks. This page is about that second part.

A construction mortgage (or construction loan) is not “just a regular mortgage with more paperwork.” The money comes out in stages, the bank will send people to your site, and the whole thing can stall if your budget, schedule, builder or land isn’t ready.

If you plan to manage trades and run the job yourself, read our guide on acting as your own general contractor so you understand what lenders expect from an owner-builder before you start talking to the bank.

This hub walks you from idea to keys:

- What a construction mortgage is

- How draws work

- Land + build, self-builds, renos, and “construction-to-permanent” loans

- What lenders actually look at

- Where projects go off the rails and how to protect yourself

Use this page as the map. Each section can be its own deeper guide later.

Why This Construction Mortgage Hub Exists

Most “construction loan” pages are written by banks trying to sell you a product, not explain the risk. This hub is the opposite. It’s written from the jobsite side first, paperwork second.

You’ll see how money actually moves from bank to builder, what happens when a draw is delayed, and why one bad quote can blow up your whole project. Land, framing, inspections, codes, cash flow – it’s all in one place so you’re not guessing in the middle of a pour.

- Real examples of how draws line up with foundations, framing, and lock-up.

- Owner-builder, custom home, and renovation paths laid out side by side.

- Plain-language warnings on the stuff that actually kills builds: appraisals, overruns, and timing.

Use this hub before you sign anything. If you understand how the loan, the plans, and the schedule lock together, you’re already ahead of most first-time builders and half the people sitting in the bank’s office.

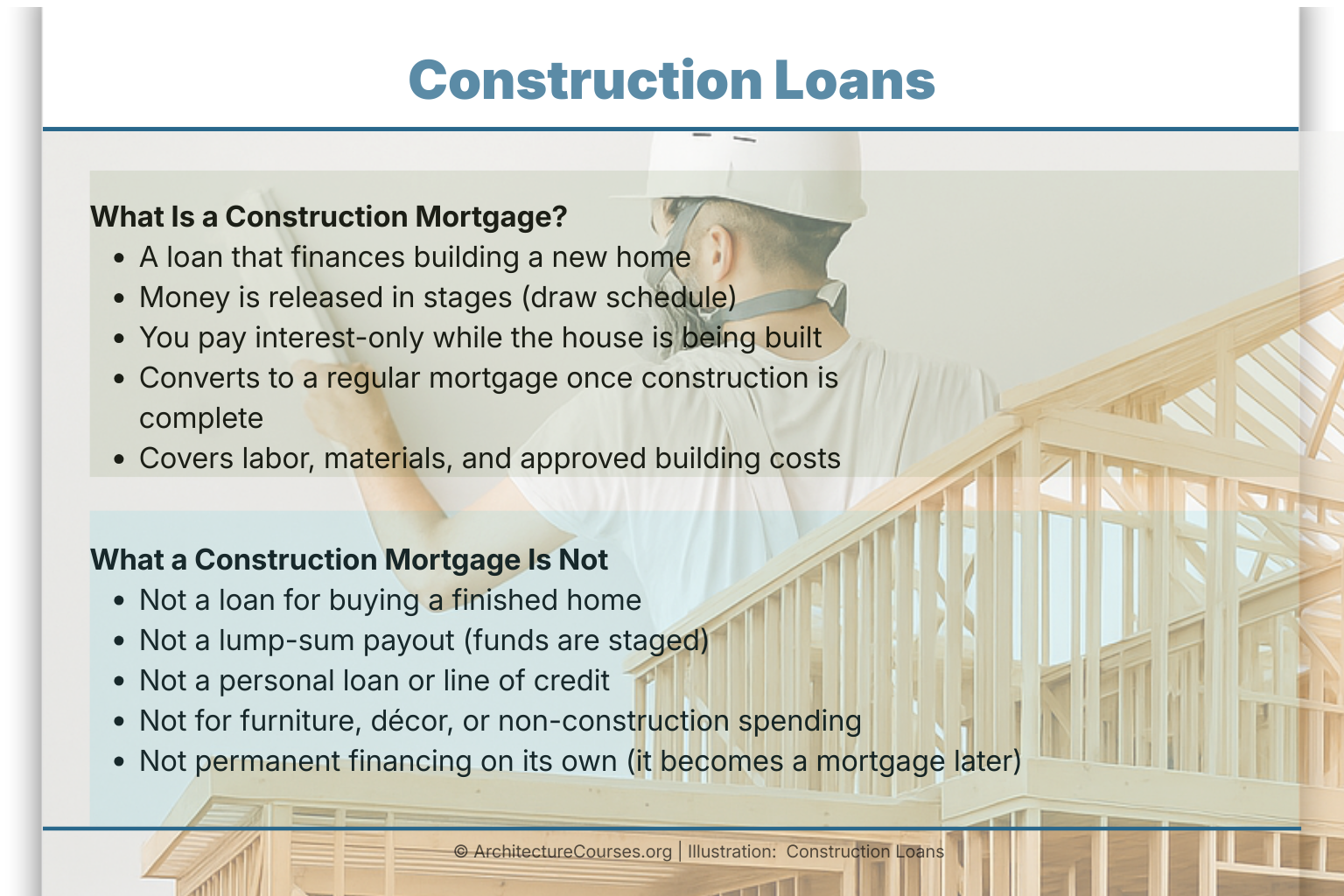

What Is a Construction Mortgage?

A construction mortgage (or construction loan) is money set up for a house that is a jobsite, not a finished home. You are building new, adding a major addition, or stripping the structure back to framing. A normal “buy and move in” mortgage does not fit that risk, so banks use a different system.

In the U.S., this is usually a construction-to-permanent loan. You start with a short construction phase where you pay interest only on what has been advanced. When the house is done and passes final checks, that same loan converts into a regular 15–30 year mortgage.

In Canada, most banks and credit unions use a progress-draw construction mortgage. The idea is the same, but the wording changes. Money comes in “draws” at set milestones, and the lender leans heavily on appraisers, inspectors, and your builder’s paperwork.

In both systems, a few rules are always there:

- You are approved on the finished home (plans, specs, and appraised “as-completed” value), not just the land.

- The bank sets a maximum based on total build cost and what the house should be worth when it is done.

- Cash comes out in draws as work is finished: land and excavation, foundation, framing and roof, lock-up, then interior and completion.

- During the build you usually pay interest only on money that has actually gone out, not on the full approved limit.

- When the house is complete and inspected, the loan rolls into a normal mortgage, or you refinance or switch lenders if that gives you better long-term terms.

A simple example: you plan a $800,000 build on land worth $200,000. The bank might approve $700,000 based on costs and value. Your first draw could be $150,000 for land and foundation, then more at framing, then at drywall, then at completion. You never see a big lump of $700,000 sitting in your account. It moves in steps as the structure comes together.

Owners use construction mortgages when they are:

- Building a custom home on land they already own or are buying

- Doing a full gut job down to studs, new layout, new systems

- Adding a major addition or a new full storey

- Knocking down an old house and rebuilding on the same lot

- Putting up a duplex, garden suite, or rental while still living on part of the property

If you are planning to run the project yourself and hire the trades, lenders will treat it as an owner-builder or self-build file. That means more conditions, more backup cash, and more questions about your experience. It is worth reading a straight, practical guide to being your own general contractor before you sign anything with the bank or a builder.

On the other hand, if you only want a new kitchen, better floors, or a non-structural facelift, a full construction mortgage is usually overkill. In those lighter cases, a refinance, HELOC, or small renovation loan often works better than a full draw schedule with inspections and holdbacks.

See also: How to Finance Building a House on Your Land

Types of Construction Mortgages & Loans

Most products fall into a few main buckets. Names change by bank and country, but the logic is similar.

Construction-to-Permanent / “One-Time Close” Loan (Common in the U.S.)

This is the classic U.S. construction-to-perm loan. You close once, build, then roll into a normal mortgage.

- One approval and one set of legal fees.

- During construction you pay interest-only on the amount advanced.

- When the home is finished, it converts to a regular principal-and-interest mortgage.

Best for: U.S. borrowers who want a single package from excavation to move-in, with less rate and paperwork risk.

Progress-Draw Construction Mortgage (Common in Canada)

This is the standard Canadian-style progress-draw construction mortgage.

- The bank approves a limit based on land + build cost and appraised “as-completed” value.

- Money comes out in staged draws as work is finished, often at:

- Land / initial advance

- Foundation

- Framing / lock-up

- Drywall / interior rough-ins

- Completion

- An appraiser or inspector signs off at each stage.

- You pay interest-only on what has actually been advanced, not the full approval.

Best for: Custom homes, rural or infill builds, larger additions where the house is basically a jobsite for months.

Completion Mortgage for New Builds

Common in subdivisions and some infill projects. Here the builder carries the construction.

- You pay deposits and sign a purchase agreement.

- The builder uses their own financing during construction.

- Your mortgage is a normal “purchase” mortgage that closes at completion.

Best for: Buying in a new subdivision, townhome or condo project where the builder controls the entire build process.

Construction-Only Loan

This is a short-term loan for the build only.

- The lender funds the construction phase through draws.

- When the house is done, you arrange a separate long-term mortgage and pay off the construction loan.

- Two closings, two sets of legal costs, but more freedom at the end.

Best for: Builders and investors who want flexibility to shop for the best take-out mortgage once the house is finished.

Self-Build / Owner-Builder Construction Loans

In an owner-builder setup, you act as the general contractor.

- You hire trades, manage schedule, and handle site decisions.

- Many big lenders either say no or ask for:

- More equity / bigger down payment

- Strong income and credit

- Real construction experience or a professional construction manager

- Expect closer review of your budget, drawings, permits, and contingency.

If you are thinking about running your own build, it helps to know what a GC actually does day to day. A practical piece like learning to manage a project as your own general contractor gives you a reality check before you walk into the bank.

Best for: Experienced trades, small builders, or serious owner-builders with time, skills, and a clear plan. Not ideal as a first weekend project.

MUST READ: If you plan to self-build, it pays to understand where money leaks on site. A field-tested book like a practical framing and construction guide helps you see how structure, labour, and materials line up against your loan draws.

Renovation & Construction Loans for Remodels

These loans cover heavy renovations rather than a bare lot.

- Used for second-storey additions, big rear additions, full gut jobs, or major structural changes.

- Variants include:

- Renovation construction loans (full draw-style financing on an existing house)

- Purchase-plus-improvements mortgages for smaller upgrades rolled into a purchase

- Special programs like FHA 203(k) in the U.S.

- Once you start moving structure and opening up ceilings and walls, lenders treat it more like a build than a paint job.

If your reno touches structure, it helps to understand how walls and ceilings actually work. A clear explainer such as a basic guide to house framing and structure makes it easier to discuss scope and cost with both your builder and your lender.

Land Loans and Land + Build Packages

When you do not own the lot yet, the financing usually splits into:

- Land-only loan: Higher down payment, shorter term, and more focus on zoning, access, and services.

- Land + build construction mortgage: One file where the lender finances the land purchase and the build as a single project.

Some people buy land first with a short land loan, then roll it into a full construction mortgage once plans, permits, and costs are nailed down. Others wrap land and build together from day one. The “right” path depends on how far along your design and budget are when you find the lot.

We’ll come back to land in more detail below.

How a Construction Mortgage Works (Step-by-Step)

This is the part most people actually search: “how does a construction mortgage work?” Here’s the real sequence, from idea to final mortgage.

Step 1: Decide What You’re Building

Start with the project type, not the bank form. Broad strokes:

- New custom home on a vacant lot

- Tear-down and rebuild on an existing lot

- Major addition or full second storey

- Heavy renovation while you live in part of the house

This choice drives everything: lender options, draw schedule, risk level, and whether you end up with a true construction mortgage or a simpler renovation product.

Step 2: Land – Already Own It or Need to Buy?

If you already own the land, the lender starts with current land value. Your equity in the lot can often count as part or all of the down payment. You still need full plans and a build budget.

If you are buying land, the bank looks at land price plus build cost versus the appraised “as-completed” value. Some lenders wrap land and construction together in one package. Others want a land loan first, then a separate construction facility.

Servicing matters. Raw land with no road, hydro, water, or sewer is still financeable, but not with every lender and usually with stricter terms.

Step 3: Design, Plans, and Budget

Banks do not lend off vibes. They lend off drawings and numbers.

Expect to provide at least:

- Site plan and house plans with reasonable detail

- A spec level (basic, mid, or higher-end finishes)

- A build budget broken into trades: excavation, foundation, framing, windows and doors, roof, siding, insulation, drywall, plumbing, electrical, HVAC, finishes, permits, and contingency

A solid builder quote or contract is much stronger than a single lump-sum guess. The appraiser will use your plans and budget to estimate the finished value, the same way they would for a completed home but with drawings instead of photos.

If you want a clearer feel for where the money goes in the structure itself, it helps to read a straight, field-level guide like House framing basics and how the main pieces add up before you lock your numbers.

Step 4: Choose a Builder or Go Owner-Builder

Next question: who is actually building this house?

With an experienced licensed builder and a fixed-price contract, most lenders relax. With a new builder, a loose quote, or an owner-builder setup, expect more questions and tighter conditions.

If you plan to act as your own general contractor, most banks treat it as higher risk. They may ask for:

- A bigger down payment or more equity

- Proof of strong income and clean credit

- A real schedule and trade list, not just “I’ll figure it out”

- Extra contingency beyond the usual 10–15%

Before you tell a lender you’ll run the job yourself, it’s worth going through a practical guide on what being your own general contractor actually involves day to day.

Step 5: Apply for the Construction Mortgage

The application looks like a regular mortgage file plus a small project manual.

You provide:

- Income documents (pay stubs, T4s, NOAs, or business financials)

- Consent for credit checks and a list of your existing debts

- Plans, budget, and the builder contract or detailed quote

- Land details: purchase agreement, MLS, survey, or proof of ownership

The lender runs the numbers:

- Credit score and history

- Debt-to-income ratios

- Whether your budget looks realistic for the design and location

- An appraisal of the “as-completed” home based on the plans

Your maximum loan is usually the lower of:

- A set percentage of total project cost (land plus build)

- A percentage of the appraised finished value

If the loan is insured (CMHC or similar), the insurance rules set the ceiling on loan-to-value and minimum down payment.

Step 6: Understand Your Draw Schedule

The draw schedule is the spine of a construction mortgage. It tells you when money actually shows up.

A typical progress-draw schedule for a new home might be:

- Draw 1 – Land / Foundation: After you close on the land and the foundation is in.

- Draw 2 – Framing / Lock-Up: Shell framed, roof on, basic openings in.

- Draw 3 – Rough-Ins / Drywall: Plumbing, electrical, HVAC, insulation, and drywall complete.

- Draw 4 – Completion: Ready for occupancy or very close.

Between draws an appraiser or inspector visits, confirms the stage, and reports percentage complete. The lender then releases funds for that stage, often holding back a small percentage until all lien periods are clear.

You need to know, in writing:

- Which stages your lender uses and what each one pays

- Who pays the inspector or appraiser fees and when

- How the draw timing lines up with your builder’s payment schedule

A good draw schedule keeps your builder paid without forcing you to cash-float large gaps. A bad one does the opposite.

Step 7: During Construction – Payments and Cash Flow

While you build, the loan usually runs as interest-only on whatever has actually been advanced.

If the total approval is $800,000 but only $300,000 has been drawn, you pay interest on $300,000, not the full $800,000. Payments are monthly or, in some setups, paid from an interest reserve set aside in the loan.

At the same time, you still need to cover:

- Rent or payments on the place you live now (if you have not sold)

- Any existing mortgage on the land

- Upgrades, changes, and extras the lender will not fund

- Inspection and appraisal fees for each draw

- Insurance, utilities, and basic security on the jobsite

For 8–18 months you are running a small construction business whether you think of it that way or not. Cash flow planning matters as much as design.

Step 8: Converting to a Regular Mortgage

At the end, the construction phase has to land as a normal long-term mortgage.

Final inspection and appraisal confirm that the house is complete and habitable. Then one of two things happens:

- Your construction-to-permanent loan automatically rolls into a standard mortgage with principal and interest payments, or

- You refinance into a new mortgage with the same lender or a different one if you used a construction-only or private loan.

You choose fixed or variable, term length, and amortization the same way you would for any normal home loan. Some lenders re-check income and credit at this stage. Others treat it as a pre-agreed conversion if nothing major has changed.

Step 9: When Things Go Wrong

The problems are predictable, but they still hurt:

- Costs jump and the project runs over budget.

- Material prices spike mid-build.

- The builder walks, goes bankrupt, or falls badly behind.

- Inspections fail and a draw is delayed.

- The final appraised value comes in lower than planned.

- Your income or debt picture changes before conversion.

When that happens, the lender may ask you to put in more cash, adjust the scope, bring in a new builder, or, in the worst case, sell the land or partly built structure to clear the loan.

If cracks or structural issues show up during or after the build, bringing in a specialist early helps. Many owners lean on a straight-talking guide like what to know before you hire a structural repair contractor so they do not make the same mistakes twice.

The best defence is boring: conservative numbers, a real contingency fund, and a builder and lender you can actually reach when something shifts.

Who Lends on Construction?

Most people start with “my bank.” In reality, construction money usually comes from five buckets. Each has its own rules, risk tolerance, and pain points.

Before you sit down with anyone, be clear on what you’re building and who is actually running the job. If you plan to manage trades yourself, it helps to read a realistic guide on acting as your own general contractor so you know what lenders will push back on.

Big Banks

In the U.S. and Canada, this means the usual names: RBC, TD, Scotiabank, BMO, CIBC, plus the big national banks on the U.S. side.

They like clean files: strong income, good credit, fixed-price contract, and a builder with a track record.

- Pros: competitive long-term mortgage rates, lots of branch and online support, easier to roll into a regular mortgage at the end.

- Cons: strict paperwork, less patience for owner-builder projects, slow to approve changes once you’re mid-build.

Field tip: ask early if they require a fixed-price contract and exactly how many draws they allow. If their draw schedule doesn’t line up with your builder’s payment milestones, you’ll end up floating the gap with your own cash.

Credit Unions and Regional Lenders

These are often friendlier to “real life” builds: rural land, odd lots, or houses that don’t look like the builder brochure.

- Pros: local staff who know typical build costs in your area, sometimes more flexible on land type and owner-builder files.

- Cons: smaller lending limits, tighter geographic areas, and they may walk away from very remote or unusual sites.

Field tip: when you talk to a credit union, bring a simple one-page summary of your project: lot, size, builder, rough budget, and timeline. It makes it easier for them to say “yes, this fits our box” or “no, try a different lender” before you waste time on a full application.

Mortgage Brokers

Brokers are matchmakers. They don’t lend their own money (usually), but they know which banks, credit unions, and specialty lenders will touch construction files.

- They can place standard builds with big banks.

- They can route trickier deals to credit unions or private lenders.

- They see which lenders actually fund on time and which ones drag their feet.

Field tip: ask a broker how many true construction or progress-draw deals they closed last year. Someone who only does vanilla purchases will not know the land, draw, and inspection traps the way a construction-savvy broker does.

Specialty Construction and Private Lenders

These are the “we’ll do it when the bank won’t” outfits: private mortgage funds, MICs, hard-money lenders, and niche construction lenders.

- Pros: fast decisions, more tolerance for unusual land, complicated projects, or bruised credit.

- Cons: higher rates and fees, shorter terms (often 12–24 months), and tighter timelines to finish or refinance.

They’re common for:

- Small infill builders doing spec houses.

- Owners who need to start quickly and refinance into a bank mortgage later.

- Projects that changed so much mid-stream the original bank pulled back.

Field tip: on any private or specialty loan, read the exit language twice. Make sure you know the exact date you must be out, any renewal fees, and what happens if the build runs long or the market softens.

Builder-Arranged Financing

Some builders offer “we handle the financing” packages. They build the house on their own credit line and you close with a regular mortgage at the end, or they send you to a specific bank that pre-approves all their buyers.

- Pros: less paperwork during construction, no draw inspections on your side, often smoother for subdivision or townhome projects.

- Cons: less control over lender choice, deposits at risk if the builder fails, and contracts that are written in the builder’s favour, not yours.

Field tip: treat the paperwork like any other construction contract. Understand how payments, extras, and delays are handled. A clear explainer on how construction contracts deal with cost and risk is worth reading before you sign anything that ties your deposit to a long build schedule.

No matter which path you pick, write down three things before you commit: who holds title at each stage, who controls the money at each draw, and what the lender can do if the project falls behind. Most “surprises” in construction financing come from not asking those questions up front.

Construction Mortgage Rates and Costs

Construction money is riskier and messier than a simple purchase mortgage, so costs are different.

Why Construction Rates Are Often Higher

Reasons:

-

The lender is funding a moving target (work in progress).

-

Market value is not as secure as a finished, occupied home.

-

There’s more admin: inspections, appraisals, draws.

Expect:

-

A rate premium over their best “headline” mortgage rate during the build.

-

Sometimes a rate adjustment when you convert to the permanent mortgage.

What You Pay

Your total cost has two buckets:

-

Interest cost

-

Charged on the drawn balance only, not the full approval.

-

Often interest-only during construction.

-

-

Fees and charges

-

Lender admin and setup fees

-

Appraisal and inspection fees (per visit)

-

Legal fees (often more than a simple purchase)

-

Land transfer tax and title insurance (if buying land)

-

Mortgage insurance premiums (if insured / CMHC-type coverage applies)

-

Some lenders set up an interest reserve inside the loan. That means a portion of the approval is earmarked to cover interest during construction instead of coming out of your pocket monthly. You’re still paying it; it’s just prepaid from loan funds.

Comparing Construction Mortgage Offers

Don’t just look at the headline rate. Compare:

-

Maximum loan-to-value (how much they’ll lend vs cost/value)

-

Required down payment / equity

-

Draw schedule (stages and percentages)

-

Inspection/appraisal frequency and cost

-

Flexibility on builder choice and owner-builder

-

Terms on conversion to permanent mortgage (rate lock, re-qualification, fees)

The “cheapest” rate with a terrible draw schedule can cost you more in stress and bridge money than a slightly higher rate with smoother funding.

Down Payment and Equity: How Much Do You Need?

Everybody wants a clean number. There isn’t one single answer, but there are patterns.

Broadly, lenders look at:

-

Total project cost (land + build + soft costs)

-

As-completed appraised value

-

Whether the loan is insured or not

Scenario 1: You Already Own the Land Free and Clear

Here your land often acts as your down payment.

Example:

-

Land worth $250,000

-

Build cost (all-in) $550,000

-

Total project: $800,000

If your lender will go to, say, 80% loan-to-value on as-completed value, and the appraisal supports $800,000, max loan is $640,000.

You already have $250,000 of land equity in the deal, so you may only need to bring enough cash to cover:

-

Cost overruns

-

Soft costs not included in the loan

-

Any gap between loan and total cost

Scenario 2: You Have a Mortgage on the Land

Here the lender looks at equity, not just value.

Example:

-

Land value: $250,000

-

Land mortgage: $150,000

-

Equity: $100,000

Same $800,000 project, but the starting position is different. The lender has to pay out the existing mortgage and then finance the build on top. Your usable equity is the gap between land value and land debt.

Scenario 3: Buying Land and Building at the Same Time

Here your down payment is usually calculated on the total package:

-

Land price + build cost = total project

-

Minimum down payment % depends on:

-

Loan-to-value ceiling

-

Whether the loan is insured or not

-

Property type and location

-

Expect lenders to require more equity for:

-

Rural or non-standard properties

-

Owner-builder projects

-

Larger custom homes that are higher than area norms

Insured construction loans (where they exist) can allow lower down payments, but with stricter rules and premiums added to the loan.

Why Lenders Refuse Low-Equity Construction Deals

From their point of view, risks stack up:

-

Build might go over budget

-

Value might come in low at completion

-

You might not qualify for the final mortgage

More equity gives them a buffer. If something goes very wrong, there is still room to sell, clear the loan, and avoid a loss.

Construction Mortgage vs Regular Mortgage vs HELOC

Most people try to dodge construction loans and “just use a mortgage and a line of credit.” Sometimes that works. Often it doesn’t.

When a Regular Mortgage + HELOC is Enough

Good fit for:

-

Light to mid-level renovations where structure stays similar

-

Cosmetic upgrades, new kitchens, new baths, non-structural wall moves

-

Projects where the house stays safe and habitable

You:

-

Refinance your current home

-

Pull out equity or set up a HELOC

-

Pay contractors directly with that money

No inspections from the bank, no draw schedule. Your risk, your control.

When You Really Need a Construction Mortgage

You’re into construction-mortgage territory when:

-

You’re building from scratch

-

You’re adding a storey or major addition

-

You’re doing a gut job where walls are open, systems are replaced, or the house is borderline uninhabitable

Here the project is too big to fund with credit cards and short lines. The lender wants to control how and when money is released. That is what a construction mortgage is built for.

Why Stacking Personal Loans is Dangerous

It looks easy:

-

Small line of credit here

-

A few 0% store cards

-

Some credit cards and a personal loan

Two problems:

-

Your debt-to-income ratio blows up and you can’t qualify for the final mortgage.

-

Short-term loans and cards have high rates and can spiral if the project runs long.

If you’re going to spend house-changing money, do it with a plan, not scattered consumer credit.

Owner-Builder and Self-Build Construction Mortgages

Everyone loves the idea of “saving the GC markup.” Lenders don’t love it as much.

What Counts as Owner-Builder?

Typically you are an owner-builder if:

-

You hold the building permit as the contractor of record, or

-

You directly hire and coordinate most of the trades, or

-

You’re doing a large amount of work yourself beyond normal DIY.

Some lenders will not touch true owner-builder projects. Others will, with conditions.

Why Lenders Are Nervous

They worry about:

-

Incomplete or unrealistic budgets

-

Poor scheduling and delays

-

Work not done to code or permit spec

They trust licensed builders with a track record more than a first-timer with YouTube and enthusiasm.

What Owner-Builders Are Usually Asked For

Common requirements:

-

Higher equity (more money down)

-

Stronger credit and income than a standard file

-

Detailed budget and schedule, sometimes using the lender’s cost breakdown form

-

Proof of contingency funds beyond the loan

-

Sometimes a requirement to hire certain trades (structural, electrical, HVAC) rather than DIY

Insurance also changes. As an owner-builder, you are responsible for site safety, liability, and workers’ compensation rules for anyone you hire.

Construction Loans for Renovations, Additions and Gut Jobs

Not every construction loan is for an empty lot.

When a Construction Loan for Renovation Makes Sense

Good candidates:

-

Adding a full second storey

-

Large rear additions with new foundations

-

Changing roof lines significantly

-

Converting single-family to duplex / triplex

-

Complete interior gut and re-build

These projects:

-

Change the value and structure of the house

-

Carry real build risk

-

Often require new permits and inspections

Lenders will treat them more like a new build, with:

-

Appraised “as-completed” value

-

Draws based on progress

-

Inspections during key stages

Renovating While You Live There

Living in the house during construction can:

-

Reduce your carrying costs (no rent on a separate place)

-

Increase site risk and stress

From a lender’s view, the big question is:

“Is this still a safe, habitable home, or essentially a jobsite?”

Once you cross into “jobsite”, construction-style oversight shows up.

Converting to a Permanent Mortgage After Renovation

At completion:

-

Appraiser confirms work and final value

-

Lender converts loan to a standard mortgage or refinances to a new product

If the value didn’t increase as much as you expected, or the project ran over budget, you may end up with less equity than planned. That can limit options or force you into a smaller refinance than you hoped.

Land + Construction: Mortgage to Buy Land and Build

This is its own problem set.

Land-Only Loans

When you buy just the land:

-

Down payment is often higher than for a house (20–35%+ typical ranges).

-

Terms are shorter.

-

Lenders care a lot about:

-

Road access

-

Zoning and permitted use

-

Servicing (water, sewer or septic, hydro)

-

Environmental issues

-

Later, you bring your plans and budget and apply for the construction mortgage that will pay out the land loan and fund the build.

Land + Build Packages

If you know exactly what you’re building:

-

You can sometimes arrange one land + construction mortgage from day one.

-

The lender approves based on the combined project.

-

First draw pays for the land (or pays out the land vendor).

-

Later draws follow the build.

Serviced subdivision lots with a builder package are the easiest version of this. Raw rural land plus a fully custom home is the hardest.

Rural and Non-Standard Land

Expect more questions and stricter terms for:

-

Private roads and shared driveways

-

Steep, rocky or heavily forested land

-

Waterfront with setbacks and conservation rules

-

Hobby farms or mixed-use setups

Lenders want to know that if they ever had to sell, they could actually find a buyer in a reasonable time.

Construction-to-Permanent Loans

If you’re reading from the U.S., you’ll see a lot of “construction-to-permanent” language.

Basic pattern:

-

One loan, one closing.

-

Interest-only during construction.

-

Automatic conversion to a permanent mortgage at completion.

Variants:

-

Conventional C2P – backed by Fannie Mae / Freddie Mac rules.

-

FHA construction-to-perm – uses FHA guidelines, often with lower down payment but more rules.

-

VA construction loans – for eligible veterans and service members.

-

USDA construction loans – for qualifying rural properties and borrowers.

You don’t need to become an expert on every U.S. program. For your readers, a single “program overview” page that names the options and clearly says “talk to a licensed loan officer for the current rules” is enough.

Getting Approved: What Lenders Look At

Underneath the product names, the approval math is pretty simple.

They look at:

-

You

-

The project

-

The property

You: Income, Credit, Debts

They want to see:

-

Stable, verifiable income (T4, salary, long-term contracts, or solid self-employed history)

-

Credit score high enough for their policies

-

Reasonable debt-to-income ratio once everything is in place

If you’re self-employed, expect more paperwork: financial statements, tax returns, notices of assessment, sometimes business bank statements.

The Project: Budget, Plans, Builder

They study:

-

Is the budget realistic for this type of build in this area?

-

Are there contingency funds built in (often 10–15%)?

-

Are plans and permits at the right stage?

-

Is the builder established, insured and experienced with this type of project?

Weakness in any of these doesn’t always mean “no”, but it pushes you toward higher equity, stricter terms, or more expensive lenders.

The Property: As-Completed Value and Market

They care about:

-

Location and resale demand

-

Surrounding home values and build quality

-

Whether your project is way over or under the local norm

If you plan the most expensive house on a modest country road, don’t expect the lender to finance 95% of your optimistic budget. They lend against market reality, not just your tastes.

Draw Schedules, Inspections and Cash Flow in Detail

Draw mechanics are where most headaches live, so it’s worth spelling out.

Typical Draw Milestones

Every lender has its own version, but for a standalone home build you’ll see something like:

-

Initial / Land – Pays land seller or refinances land loan.

-

Foundation – Excavation, footings, foundation walls, backfill.

-

Framing / Lock-Up – Structure up, roof on, windows/doors installed.

-

Interior Rough-Ins / Drywall – Plumbing, electrical, HVAC, insulation, drywall.

-

Completion – Interior finishes done, exterior complete, occupancy possible.

The lender assigns a percentage of total funds to each stage. The appraiser confirms that stage is complete before they release the next chunk.

What Inspectors Look For

They check:

-

Work completed vs the stated stage

-

Obvious defects or safety issues

-

Whether the project still lines up with original plans

They do not usually do a code inspection—that’s the job of the building department. They’re there to answer “Is this stage complete enough to justify the next draw?”

When the Draw Is Delayed or Reduced

It can happen if:

-

Work isn’t as far along as you or the builder thought

-

There are visible problems

-

Market conditions or appraised value change

When a draw is delayed, you still have bills. Options:

-

Use savings or a backup line of credit to bridge

-

Negotiate with the builder for a short delay in payment

-

Push to correct the issue quickly and re-inspect

This is why keeping buffer cash outside the construction mortgage is so important.

Risk, Problems and Worst-Case Scenarios

You build trust by being honest about what can fail.

Common problems:

-

Overruns – materials, labour, or design changes push costs beyond budget.

-

Delays – weather, trades, permits, or supply chain.

-

Builder issues – disputes, poor quality, or business failure.

-

Value issues – final appraisal comes in lower than expected.

-

Life changes – job loss, illness, separation mid-project.

Practical defenses:

-

Realistic budget with contingency (not just a token number).

-

Fixed-price or clearly defined contract where appropriate.

-

Builder references and real due diligence.

-

Keeping your personal finances simple during the build (no new car loans, no surprise credit card binges).

-

Conservative expectations on final value and future rates.

If you treat a construction mortgage like a business project instead of a Pinterest mood board, you stand a much better chance of getting from empty lot to working kitchen without running out of money halfway.

Country-Specific and Program-Specific Guides (Where to Go Deeper)

You don’t have to cram every program into this page. Instead, spin out focused guides that this hub links to, for example:

-

VA / FHA / USDA Construction Loans: Quick Overview for U.S. Owners

-

Construction-to-Permanent Loans in the U.S.: One-Time Close vs Two-Time Close

-

CMHC and Insured Construction Financing: What Changes for New Builds

-

Construction Mortgage in Canada: Progress-Draw Basics for Homeowners

-

Owner-Builder Construction Mortgage (Canadian Guide)

Each of those can carry the product-specific fine print and official references.

FAQ

1. Is it harder to get a construction mortgage than a normal mortgage?

Yes. The lender has to underwrite you, the land, the builder, the plans, and the budget. There are more moving parts and more ways the project can fail, so they want stronger files and more equity.

2. Do I pay interest on the full loan from day one?

No. You normally pay interest only on the amount that’s been advanced so far, not the total approved limit. If half the money has been drawn, you pay interest on that half.

3. Can I use my land as a down payment?

Often, yes. If you already own the land, its current value minus any mortgage on it is your equity. Many lenders let that count toward your required down payment on the total project.

4. Who pays the builder – me or the bank?

The lender advances draws to your lawyer or sometimes to you, and from there, funds go to the builder according to your contract. The bank doesn’t write cheques directly to the framer. You’re still the one managing the relationship and signing off on invoices.

5. Can I switch builders in the middle of the project?

You can, but it’s messy. The lender will want:

-

New contracts

-

Updated budgets and schedule

-

Sometimes a fresh appraisal

Expect some downtime while paperwork catches up, and be ready for disputes with the old builder over what’s been paid for.

6. Can I live in the house while I finish it?

It depends on the stage and safety. Some lenders allow occupancy once core systems are in and inspected; others want the project substantially complete first. From a practical standpoint, living in half a jobsite is hard on families and can slow trades down.

7. Can first-time home buyers use a construction mortgage?

Yes, in many cases. But as a first-timer, you have to be even more realistic about budget, time, and stress. Some programs and incentives can be used for new builds, but you need to check the rules carefully with a broker or advisor.

8. What happens if the final appraisal is lower than expected?

If the finished home appraises lower than your plan, the lender may:

-

Lower the maximum permanent mortgage

-

Ask you to put in extra cash to reduce the loan

-

Push you toward a different product or term

This is why you don’t want to be right at the edge on both budget and equity.

9. Is fixed or variable better for construction loans?

There isn’t one right answer. Many people:

-

Accept whatever construction rate structure the lender offers during the build, then

-

Decide on fixed vs variable at conversion time based on rates and risk then.

Some one-time-close loans lock a long-term rate up front. That protects you from rising rates but can limit flexibility. It’s a trade-off.

10. How long do I have to finish the build?

Construction periods are usually 6–18 months, depending on lender and project. If you go far past the agreed term, the lender may charge higher rates, fees, or even demand changes to the loan. Build a realistic schedule and add buffer.

References and Official Resources

You’re dealing with real money, permits and safety. Always cross-check what you read here with current official guidance and a licensed mortgage professional where you live.

United States – Official Construction & Mortgage Guidance

- Consumer Financial Protection Bureau (CFPB) – plain-language guides on mortgages, construction loans and closing costs.

CFPB – Owning a Home tools and mortgage explanations - U.S. Department of Housing and Urban Development (HUD) – FHA-backed loans, including construction and rehab programs.

HUD – Single Family Housing Programs (FHA-backed mortgages and construction-related options) - Federal Housing Administration (FHA) – details on insured mortgages, including one-time-close and rehab programs that affect new builds and major renos.

FHA / HUD – 203(k) Rehab and Construction-Related Mortgage Info - U.S. Department of Veterans Affairs (VA) – official guidance on VA-backed construction and permanent loans for eligible veterans.

VA – Home Loan Types (including construction and renovation options) - U.S. Department of Agriculture (USDA) – rural housing and construction programs for eligible areas and borrowers.

USDA – Single-Family Housing Programs (rural construction and new home financing)

Canada – Construction Mortgages, Codes and Housing Agencies

- Canada Mortgage and Housing Corporation (CMHC) – national housing agency with information on insured mortgages, self-build and new construction financing rules.

CMHC – Homebuying and Mortgage Basics (including building and new construction) - Financial Consumer Agency of Canada (FCAC) – neutral, government-backed explanations of mortgages, construction costs and borrowing limits.

FCAC – Mortgage Guides and Tools - National Building Code of Canada – model code that provinces use or adapt; new builds and major renovations must follow a version of this.

National Building Code of Canada – Official Access - Ontario Building Code (example provincial reference) – if you are building in Ontario, this is the legal standard for your plans, permits and inspections.

Ontario Building Code – Current Consolidated Regulation - FSRA – Financial Services Regulatory Authority of Ontario – regulates mortgage brokers, lenders and administrators in Ontario.

FSRA – Mortgage Consumer Resources

Building Codes, Safety and Professional Guidance (General)

- International Code Council (ICC) – publishes the International Residential Code (IRC) and International Building Code (IBC), widely used or adapted across the U.S. and in other countries.

ICC – Official Code Library (IRC, IBC and related codes) - National Fire Protection Association (NFPA) – codes and standards that affect electrical work, life safety and some aspects of building design.

NFPA – Codes and Standards Index - Building Science Corporation – widely cited building science resource on moisture, insulation, roofing and wall assemblies that matter to lenders and appraisers.

Building Science Corporation – Technical Articles

Professional & Trade Associations (Builders, Appraisers, Mortgage Pros)

- Canadian Home Builders’ Association (CHBA) – represents builders and renovators across Canada; good starting point if you want a contractor used to bank draws and inspections.

CHBA – Find a Home Builder or Renovator - National Association of Home Builders (NAHB – U.S.) – resources on new home construction, codes and builder best practice for American projects.

NAHB – New Home Construction Resources - Appraisal Institute of Canada (AIC) – professional body for Canadian appraisers; appraisals are central to “as-completed value” on construction loans.

AIC – About Appraisers and Property Valuation - Appraisal Institute (U.S.) – similar role for U.S. appraisers handling new builds, infill projects and complex properties.

Appraisal Institute – Property Appraisal Resources - Mortgage Professionals Canada – national association for Canadian mortgage brokers and lenders.

Mortgage Professionals Canada – Find a Licensed Mortgage Broker

Use this hub to understand how construction financing fits with land, design and the build itself. Then use these official sites – plus a licensed mortgage professional in your province or state – to confirm the current rules, products and numbers before you sign anything.